It might be months before Federal Reserve authorities are prepared to take any action on rates of interest, so traders are concentrating on something else that normally gets less attention: The undercarriage, or pipes, of financing markets, where things might begin to go awry in particular situations and weaken self-confidence in the U.S. banking system.

Big monetary companies like money-market funds and banks utilize over night programs such as the Fed’s reverse repurchase center to park big quantities of money on a short-term basis. They do so through deals referred to as reverse repos, which include the quick exchange of money for top quality securities like Treasurys that are on the reserve bank’s balance sheet, briefly decreasing the supply of reserve balances in the banking system.

This pipes is what assists the Federal Reserve keep its primary policy rate target in check and enables markets to operate more efficiently. It becomes part of a procedure that normally runs silently in the background of monetary markets, however probably might wind up ending up being as disruptive as it remained in September 2019 when volatility grasped the over night financing market in the middle of a huge decrease in bank reserves.

The year 2019 “was one example of what might take place once again, when banks faced reserve shortage, and it was a circumstance that was unfolding really quickly and showed to be really disruptive for the banking system,” stated financial expert Derek Tang of Monetary Policy Analytics in Washington.

” It was rather tough for Fed authorities to find out what to do in genuine time. If it takes place once again, they may be much better ready, however it is uncertain if any of their actions would suffice to balance out the danger.”

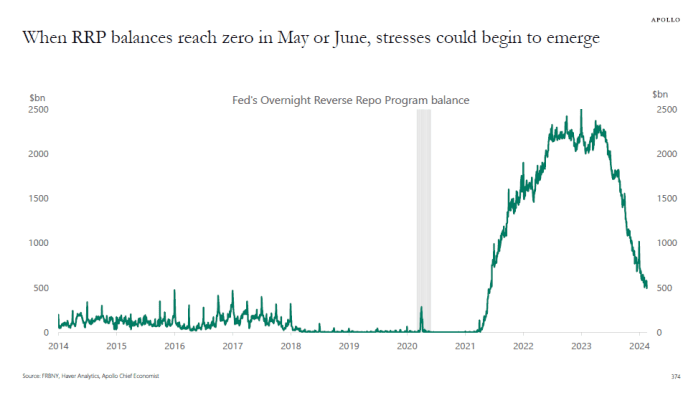

At the minute, use of the reverse-repo center is decreasing, with the quantity of day-to-day balances diminishing to simply under $570 billion since Wednesday from as high as $2.55 trillion on Dec. 30, 2022. The worry is that as soon as RRP use drops to absolutely no, an environment might emerge in which banks no longer have plentiful reserves, and these issues are growing simply ahead of the 1 year anniversary of Silicon Valley Bank’s collapse.

In the meantime, nevertheless, bank reserves are still holding up even as RRP use is diminishing. Reserves are the very little quantities of money that organizations are needed to have on hand to fulfill Fed requirements in case of unforeseen and big needs for withdrawals. California-based Silicon Valley Bank collapsed last March after a lot of clients pulled deposits at approximately the exact same time, producing a timeless bank run that threatened to shatter self-confidence in the U.S. banking system and required regulators to reinforce their oversight.

Up until now this year, financing markets have actually displayed little bit– if any– indication of the stress seen in late 2023, according to John Velis, an Americas macro strategist for BNY Mellon. In 2015’s stress took the kind of a November spike in short-term loaning rates within the over night financing market, followed by a repeat in December. Tensions have not appeared in this corner of the monetary market as they did at the end of in 2015, and liquidity seems adequate in the meantime, Velis composed in a note today.

As long as bank reserves stay plentiful, this provides the reserve bank more freedom to continue decreasing the size of its $7.58 trillion balance sheet, under the procedure referred to as quantitative tightening up. The Fed has actually been utilizing QT to tighten up monetary conditions and to drain pipes liquidity out of the system, with much of that effort appearing in falling RRP use rather of bank reserves up until now.

” When RRP reaches absolutely no in Might or June, there might no longer be plentiful reserves in the banking sector, which increases the likelihood of a mishap someplace in the pipes of the monetary system,” stated Torsten Slok, primary financial expert at Apollo Global Management in New York City. In a note over the weekend, he mentioned possible effects such as “less assistance for T-bills [Treasury bills], period, and credit markets, or tensions in cash markets comparable to what we saw in September 2019.”

According to Tang, the financial expert from Monetary Policy Analytics in Washington, “all of these problems are assembling at the Fed’s balance sheet, which is the location or website where these policies are chosen and which streams through to monetary conditions. So the moving parts are what interest the marketplaces.

” Individuals hesitate that there’s a calm before the storm. Simply put, things work till they do not,” he stated. Via phone, Tang stated that “2024 was constantly going to be the time Fed authorities would likely review their balance-sheet strategies, so, logistically, it makes good sense that if Fed authorities are stagnating on rates of interest, that possibly they have more time to commit to these other problems.”

The minutes of the Fed’s Jan. 30-31 conference kept in mind that numerous policymakers discussed March 19-20 as a possible time to hold a thorough conversation that would assist direct them on an ultimate choice to decrease the speed of QT, or speed at which the size of the Fed’s balance sheet is diminishing. Issues about preserving sufficient bank reserves will likely figure out the Fed’s thinking on when to slow, and ultimately stop, QT.

However Velis of BNY Mellon questioned the requirement for such a conversation quickly, mentioning a present “lull” in current advancements that’s mainly attributable “to policy unpredictability, with expectations of upcoming rate cuts having actually been pressed deeper into the year.”

” Offered consistent repo rates this year, a lull in RRP drain this month, and still-quite-abundant reserves, one may question why this conversation on decreasing the speed of QT is happening,” Velis stated. He contributed to this list of advancements alleviating issues about the so-called basis trade, a method which hedge funds have actually benefited on the distinctions in rates in between Treasurys and Treasury futures. These advancements “are all part of the exact same ball of wax” and indicate less loaning in Treasurys, according to the strategist.

On Wednesday, the bond market stayed reasonably consistent after a modest down modification to fourth-quarter U.S. GDP, with traders expecting Thursday’s release of the Fed’s favored inflation gauge, referred to as the personal-consumption expenditures rate index, for January. The policy-sensitive 2-year rate

BX: TMUBMUSD02Y.

fell 6.6 basis indicate a one-week low of 4.646%, while the standard 10-year yield.

BX: TMUBMUSD10Y.

dropped 4.1 basis indicate 4.273%.

” Financiers are truly conscious that things which were going on in the background over the last 1.5 to 2 years are now possibly going to alter, and changes can constantly be possibly untidy,” stated Will Compernolle, a macro strategist for FHN Financial in New York City.

Source v.