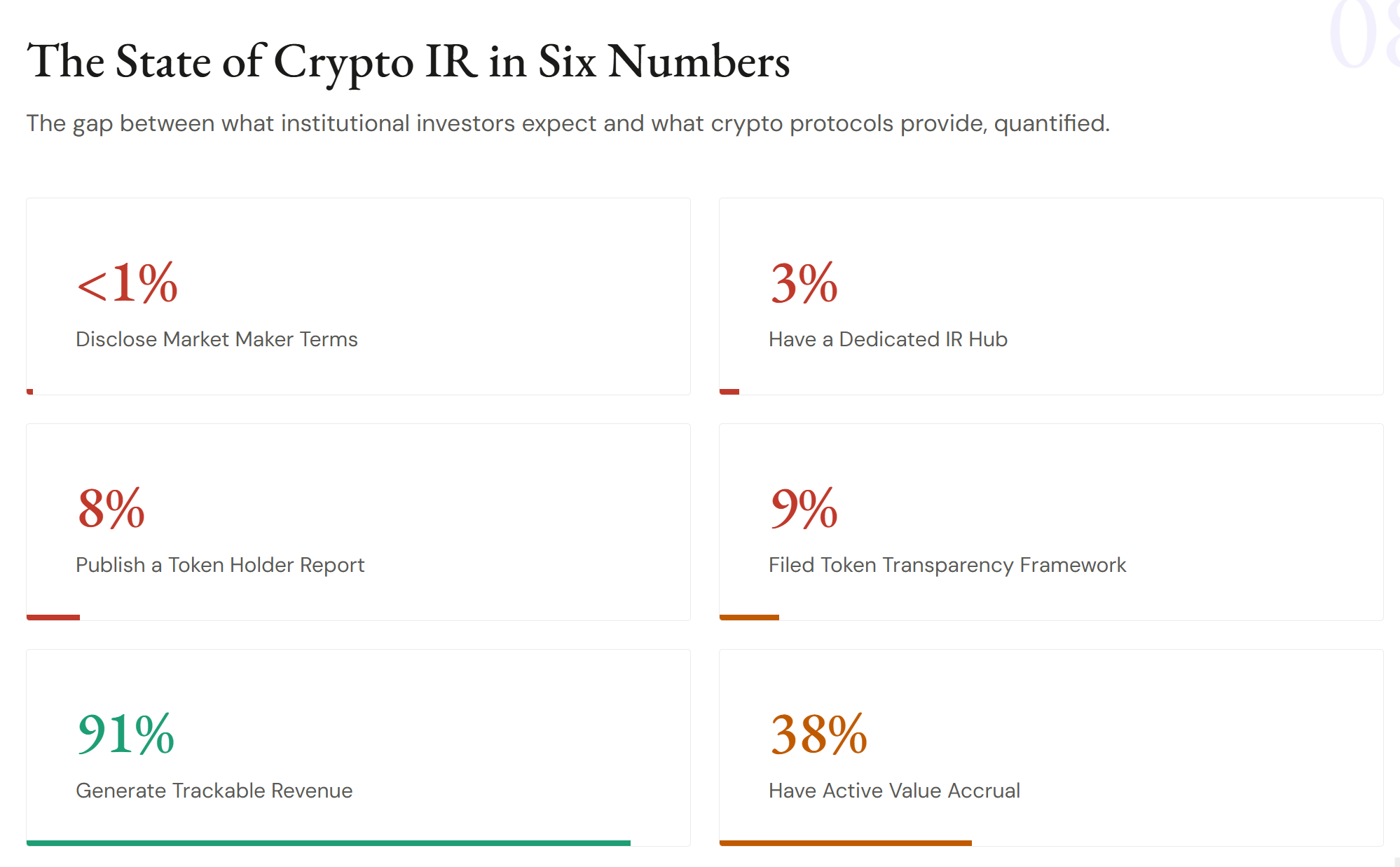

An evaluation of more than 150 significant crypto procedures reveals that disclosure of market-making plans is practically nonexistent, in spite of their main function in token trading.

The research study, carried out by crypto advisory business Novora, discovered that less than 1% of procedures reveal any terms associated with market makers. Throughout the complete dataset, just one procedure, decentralized liquidity platform Meteora, was discovered to have actually openly divulged information of its market-making plans, pointing out the task’s 2025 Yearly Token Holder Report.

The research study covered leading sectors, consisting of decentralized exchanges, providing platforms, continuous futures, layer-1 and layer-2 networks, bridges and central exchange tokens, with procedures varying in size from approximately $40 million to $45 billion in totally watered down evaluation.

Novora stated the procedures were evaluated utilizing a binary openness structure covering disclosure practices and third-party information protection, with checks versus public sources consisting of Artemis, Token Terminal, Dune, DefiLlama and Blockworks Research Study.

” This is the single most substantial openness space in the market,” Novora creator Connor King composed on X, stating that such product arrangements are consistently divulged in standard markets. “In crypto, every market individual runs without this info,” he included.

Related: Polymarket broadens into equities and products with Pyth rate feeds

Crypto’s financier reporting space

The finding indicate a wider financier relations (IR) space in crypto. Novora stated 91% of the procedures it examined created trackable earnings, however just 18% released quarterly updates and simply 8% provided token holder reports, recommending the information exists however is hardly ever packaged into structured financier interaction.

At the very same time, third-party analytics facilities has actually grown, with protection rates surpassing 85% throughout significant platforms, recommending the underlying information is extensively available however hardly ever formalized in reporting.

Sector-level breakdowns reveal unequal openness. Continuous futures procedures and decentralized exchanges tend to lead on disclosure and worth accrual systems, while L1 and facilities tasks lag in spite of bigger market capitalizations.

Related: United States crypto wash trading case reaches court as 3 extradited, 10 charged

Market-maker offers draw examination

Nontransparent market-maker plans have actually long sustained examination in crypto, specifically around token loan structures that critics state can produce rewards to discard obtained tokens into the marketplace. The United States Securities and Exchange Commission (SEC) has actually even formerly charged so-called crypto market makers with rate control.

As Cointelegraph reported, some market-maker plans are improperly structured and can rapidly turn hazardous. One extensively utilized plan, the “loan alternative design,” includes tasks providing tokens to market makers who then release them for liquidity arrangement and trading activity, typically connected to noting arrangements.

In practice, critics state this structure can produce strong rewards to offer obtained tokens into the marketplace, activating rate decreases that benefit the marketplace maker while leaving early-stage tasks with weakened liquidity and harmed token efficiency.

Publication: Bitcoin’s ‘greatest bull driver’ would be Saylor’s liquidation– Santiment creator